While there were intense backroom negotiations over certain provisions that got dropped, such as a proposal to have women register for the draft, the basic idea underlying the bill — that we should always and forever spend spectacular amounts of money on guns, bombs, tanks, planes and ships — is simply not a matter of debate.

The contrast with how we treated the far less costly bills Democrats have recently advocated, particularly the infrastructure law and the Build Back Better bill, could not be more stark.

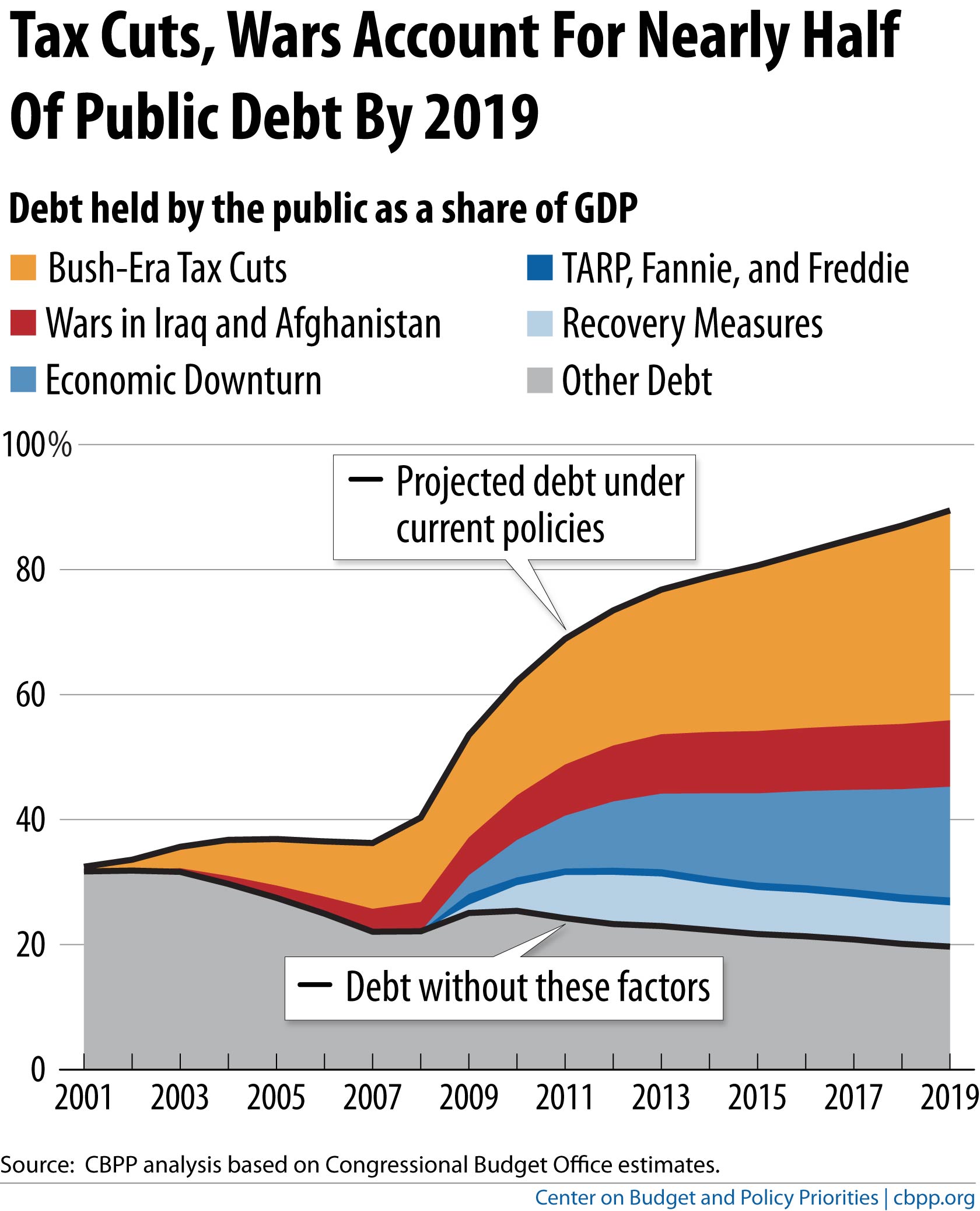

We spent endless TV hours and newspaper column inches debating the precise size of those bills and how they would be paid for. Is $3.5 trillion too much? How about $1.9 trillion? Would $1.7 trillion work? Should we increase taxes on the rich to fund them, and if not, where do we get the money?

Nobody ever asks “Where do we get the money?” when it comes to a defense bill. And that $768 billion? It’s a single year’s figure, unlike the 10-year totals that are used to describe infrastructure and BBB.

So I did some quick calculations based on previous spending. If the defense budget were to rise 4 percent a year (about what it has over the past couple of decades), 10 years from now we’d spend $1.1 trillion a year . . .

But here’s what you won’t see: headlines about how Congress is voting for a projected $9 trillion in spending oh my god!

You will not hear that from Sen. Joe Manchin III (D-W.Va.). You will not hear that from any Republicans, of the ordinary conservative or more extreme T____ist variety. You will not hear it from the sage pundits on the Sunday shows.

No one will talk about how irresponsible it is to spend like a drunken sailor, no one will cry that it’s terribly cruel to saddle our children and grandchildren with so much debt, and no one will warn darkly that such spending will surely send inflation rocketing upward.

Conservative Republicans are ranting angrily about the fact that Senate Minority Leader Mitch McConnell (R-Ky.) made a deal with Majority Leader Charles E. Schumer (D-N.Y.) to raise the debt ceiling, as though it betrays everything conservatives are supposed to believe in. If you asked them how that concern applies to the defense spending bill, they’d either look at you like you were mad or just say they’re committed to making sure the American military is the finest in the world.

Which reveals a fundamental truth: Nobody thinks we should worry about debt or potential economic consequences when it comes to the spending they happen to like. It’s only when we’re talking about things they don’t want to spend money on at all that they marshal those arguments.

There has long been a collective agreement that we’ll simply exempt military spending from those kinds of budgetary worries. Everyone just assumes that spending as much on the military as on everything else we decide to do on a year-to-year basis is just how things work. We usually spend at least half our discretionary budget on the military (mandatory spending, which includes Social Security and Medicare, is a different category).

Nor do we ever have a real discussion about what the military ought to be for. We might debate whether a particular war was a bad idea, or whether we ought to be less eager to launch full-scale invasions, but we don’t debate the fact that even referring to this spending as “defense” is a kind of self-delusion.

That’s because only a small portion of the military budget is about “defense” in any meaningful sense. Instead, it’s about maintaining our ability to project our power outward. F-35 fighter jets (total cost: $1.6 trillion and climbing) are not patrolling the skies over California and New Jersey to watch for a foreign invasion.

All those personnel (1.3 million active duty, another 750,000 or so civilians, and hundreds of thousands of contractors) spend most of their time working and training for operations that we assume will take place outside our shores. We maintain hundreds of bases in dozens of countries. We define our “security” in a way that is profoundly different from nearly every other nation, in that we conceive of it as something that is won and lost elsewhere.

There are plenty of people who consider that perfectly appropriate. But the point is that we almost never debate whether that’s what we actually want, or how much we should be spending on the military relative to the other things we’d like to do with our money.

There’s an old lefty bumper sticker that reads, “Imagine if the schools had all the money they need and the Air Force had to hold a bake sale to buy a bomber.” It’s funny because it’s absurd. But it represents a choice we made — and one we continue to make, without much public debate, every year. . . .

You must be logged in to post a comment.