When did we stumble into the dumbest timeline? Maybe we did it in 1914 when the European powers blundered into a devastating world war. Maybe it was in 1964 when Barry Goldwater accepted the Republican nomination for president while claiming that “extremism in defense of liberty is no vice”. Or maybe it wasn’t until 2016 when a demagogic con man eked out a victory in the Electoral College. Regardless of when we got here, there’s strong evidence that that’s where (or when) we are. Jonathan Chait of New York Magazine offers two pieces of evidence:

First, the demise of Biden’s social policy agenda:

The most depressing thing about the demise of the Biden administration’s social-policy agenda — other than the demise itself, of course — is the atmosphere of sheer economic illiteracy that surrounded it. Critics of the measure, ultimately including Joe Manchin, made arguments against it that were not so much misguided as lacking any elemental grasp of the basic principles involved (“not even wrong”).

The main argument used against Biden’s plan was that it would worsen inflation, with conservatives scolding Biden for ignoring the sage insights of Larry Summers. To take just one example, pundit Marc Thiessen wrote that Biden signed an economic stimulus in March 2021 “despite warnings from even liberal economists, such as former Treasury secretary Lawrence H. Summers…. But instead of trying to tamp down the flames, Biden keeps trying to pour gasoline on the inferno, with more spending and more free money from Washington.” The tone of this column, like many of the right-wing polemics, is one of incredulous condescension: Biden is such a blithering idiot that he is ignoring the obvious conclusion and instead digging holes and pouring gasoline or whatever.

Whatever the case against Build Back Better, this was not it. The American Rescue Plan did contribute to inflation; its purpose was to stimulate demand by injecting deficit-financed spending into the economy. Build Back Better had a different purpose: to address social needs over a long period of time and finance that spending through taxation.

Spending financed by new taxes is not inflationary. That is why Summers himself endorsed Build Back Better. Yet [reactionaries] spent the better part of a year citing Summers as the authority on why Biden’s long-term plans would cause inflation, oblivious to the fact that any economist, very much including Summers, would say otherwise.

In deference to public concerns about inflation, Manchin ultimately reshaped the last version of the bill as an anti-inflationary measure. The plan would have raised $1 trillion in new revenue (or reduced spending) and used half the proceeds for deficit reduction. This would not have had a large effect on inflation, but there is no question that … it would place downward pressure on prices.

[Republicans] simply refused to acknowledge this aspect of the plan at all. In the end, even Manchin himself abandoned his own plan, which was designed in part to reduce inflation, on account of inflation, which is like deciding not to cut greenhouse-gas emissions because it’s too hot.

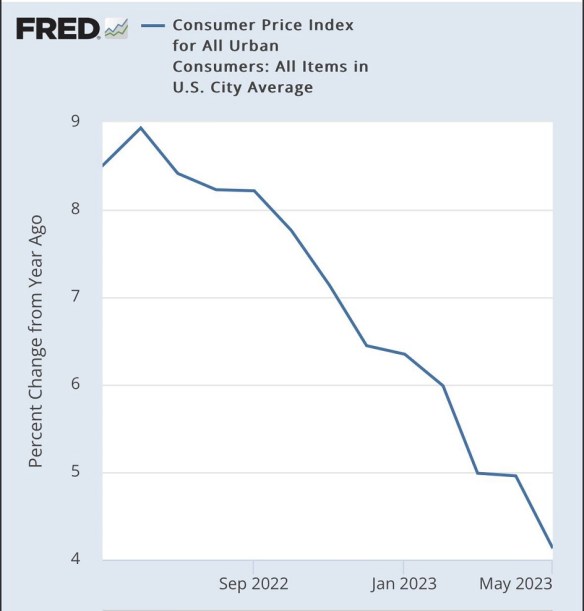

… When the 9.1% inflation number was released, Manchin [supposedly] said to Schumer, “Why can’t we wait a month to see if the numbers come down? How do you pour $1 trillion on that tempo with inflation?

Remember, $1 trillion is not the size of the spending in the bill; $1 trillion is the size of the revenue. That’s the pay-for aspect of the bill Manchin insisted on maintaining in order to fight inflation. The $1 trillion would not be poured onto economic growth. It would be poured out of economic growth.

In the end, Biden’s attempt to enact permanent social change died in an atmosphere in which the most ignorant fallacies carried the day.

Next, incoherence and derangement on gay marriage:

In 2004, the Republican Party was united in anger at the idea that judges would seize the issue of gay marriage from its rightful place in the legislative arena…..“The only question is whether the constitutional status of marriage will be determined by unelected judges or the American people,” claimed the Alliance for Marriage.

[Republicans] may finally get their wish. The matter of gay marriage is finally coming for a vote before what they have always insisted is its rightful venue: Congress. And yet, far from expressing gratitude that Congress is finally exerting its sacred Article III powers, conservatives are angry that elected officials are now meddling in business properly settled by the courts…..The old danger of activist judges has passed, and now conservative principle requires the party to take a stand against activist … legislators.

Congress is voting to codify same-sex marriage because the Supreme Court’s decision overturning Roe v. Wade undercut the main legal theory that supported other unenumerated rights, including marriage equality….

It wasn’t long ago that opposition to gay marriage held pride of place atop the ideals of the right-wing firmament, second only to the strategic genius of the Bush administration’s “global war on terror” strategy. Conservatives thundered daily against the horrific terrors that would ensue if gay people were permitted to wed each other….

After their heroic stand at the gates of civilization failed, essentially none of the things conservatives warned would happen actually transpired. The cycle of failed prophecy is a familiar one for American conservatism. Every new social or economic reform, from the abolition of child labor to the establishment of Social Security to Obamacare, brings hysterical predictions of collapse that eventually give way to silent acceptance without any stage of reconsidering the failed mental model that produced the erroneous fears in the first place.

At the moment, the case against gay marriage has reached an awkward phase. Marriage equality has enough broad acceptance (around 70 percent support) that the party doesn’t wish to emphasize the issue. But the minority in opposition forms a large enough portion of their base that few Republicans wish to renounce their old stance completely.

Hence the incentive to declare the matter an improper subject for public debate. Unable to take a stand either in favor or against the marriage-equality bill, Republicans are instead directing their arguments … against the Democrats for bringing it up at all….

Finally, an exchange on Twitter between a right-wing blogger and a history professor:

Blogger: Remember when they spent years telling us to panic over the hole in the ozone layer and then suddenly just stopped talking about it and nobody ever mentioned the ozone layer again? This was also back during the time when they scared school children into believing “acid rain” was a real and urgent threat.

Professor: The ozone hole and acid rain. Two things that were LITERALLY fixed by science-led, globally-coordinated, long-term, concrete international action. It’s like being held hostage by the world’s stupidest serial-killer.

You must be logged in to post a comment.