Economist Paul Krugman replies to confused readers:

Whenever I write about debt and deficits, I receive the same letter — OK, not exactly the same letter, but a number of letters with more or less the same gist. They read something like this: “If I borrow money from the bank, the bank expects me to pay the money back. Why isn’t the same true for the government? Why can we keep borrowing when we already owe $31 trillion?”

Just about every economist will reply that it’s misleading to make an analogy between household and government finances. But it seems to me that we often aren’t clear enough about why, perhaps because we don’t say it bluntly enough. So here’s the difference: You are going to get old and eventually die. The government isn’t.

I don’t mean that governments are immortal. Nothing is, and no doubt someday America will, as Rudyard Kipling put it, be “one with Nineveh and Tyre.” But individuals face a more or less predictable life cycle in which their earnings will eventually dwindle.

And lenders therefore demand that individual borrowers pay off their debts while they still have the income to do so.

Governments, on the other hand, normally see their revenues rise, generation after generation, as the economies they regulate and tax grow.

Governments, then, must service their debts — pay interest and repay principal when bonds come due — but they don’t necessarily have to pay them off; they can issue new bonds to pay principal on old bonds, and even borrow to pay interest as long as overall debt doesn’t rise too much faster than revenue.

In fact, when governments for one reason or another run up large debts, it is, as far as I can tell, unusual to pay those debts off.

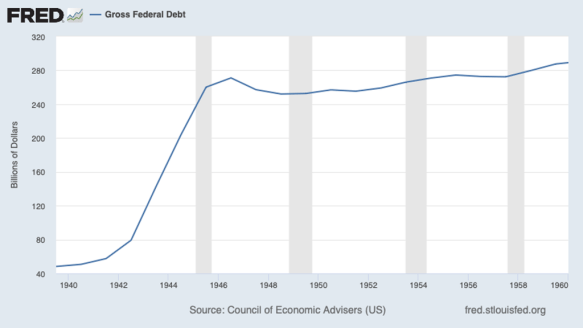

The most famous example, albeit one that many people apparently don’t know about, is the debt America incurred to fight World War II. By the war’s end, this debt was around 100 percent of gross domestic product — roughly comparable to the debt level today. So how did we pay off that debt?

We didn’t. John F. Kennedy entered the White House with federal debt roughly the same as it was on V-J Day. [This shows the gross federal debt between 1940 and 1960 — I assume adjusted for inflation.]

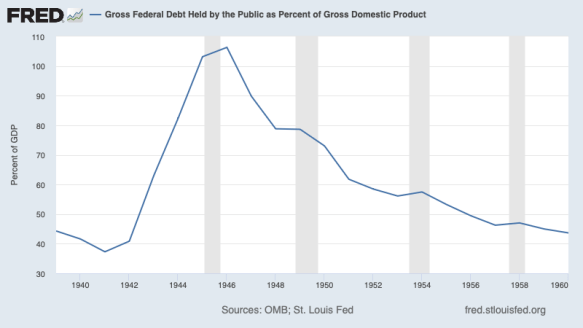

Why, then, wasn’t the 1960 election dominated by questions of how to pay off the national debt? Because while the dollar value of debt hadn’t gone down, economic growth and modest inflation meant that the ratio of debt to [Gross Domestic Product] had fallen by half. [This shows the same period, 1940 to 1960.]

For all those whose instinct is to assume that a responsible government would, like a responsible individual, pay off its debts as soon as it can, again: Governments aren’t like people. If death and taxes are the only sure things in life, well, death isn’t an issue for governments, and taxes are an asset — a growing asset — rather than a liability.

Unquote.

Of course, it isn’t exactly true that old debts aren’t paid off. The government is constantly paying investors interest on the government bonds and notes they’ve purchased, and those bonds and notes eventually mature, making old debts disappear. But investors are buying new bonds and notes at the same time (which will eventually be paid off as well).

You must be logged in to post a comment.