Paul Krugman is Distinguished Professor of Economics at the Graduate Center of the City University of New York and a columnist for The New York Times. He knows what he’s talking about but admits mistakes (this is from his Times newsletter):

Back in 2010 a group of conservative academics, economists and money managers signed an open letter warning that the efforts of the Federal Reserve to support the economy would be dangerously inflationary. But the inflation never came. So four years later, Bloomberg reached out to as many of the signatories as it could, to ask what happened.

Not one was willing to admit having been wrong.

I don’t want to be like those guys. So I’m currently spending a fair bit of time trying to understand why my relaxed view of inflation early last year has been refuted by events. What I want to do today is share where I am now on that topic and what my current take says about future policy.

Last spring the debate was focused on the American Rescue Plan, the Biden administration’s large spending package. A number of economists, including Larry Summers, Olivier Blanchard and Jason Furman, warned that it would overstimulate the economy — that output and employment would soar to levels that would create a lot of inflationary pressure.

Those of us on the other side argued that the risks of excess spending were much less than they warned — that large parts of the Biden package, like aid to state and local governments, would end up being disbursed gradually over time and therefore not have that much of an inflationary impact. To use the jargon, I argued that the [American Rescue Plan] would have a low “multiplier” [The multiplier effect measures the impact that a change in investment will have on final economic output, so that a low multiplier means less inflation.]

So here’s the funny thing: The multiplier does indeed seem to have been low. The economy has expanded fast, but it started in a deep hole and at this point is still if anything a bit below its pre-pandemic trend.

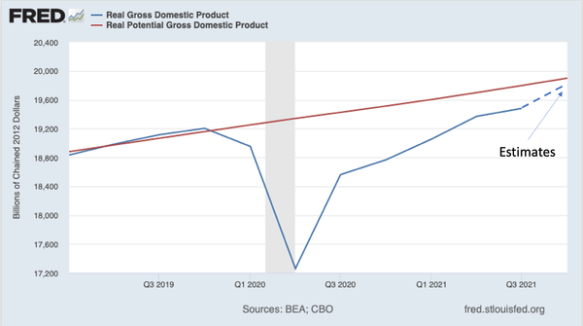

Here, for example, is real gross domestic product:

The Congressional Budget Office regularly publishes projections of “potential” G.D.P. — the level of output consistent with stable inflation. So far the official numbers through the third quarter of 2021, extended by private estimates of growth in the fourth quarter, still put us slightly below what we thought the economy’s potential was going to be.

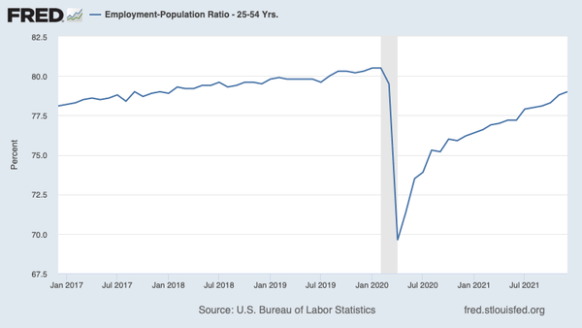

Here’s another number, the employment rate of prime-age adults, which has generally been a good indicator of the state of the labor market (probably better than the unemployment rate):

We’ve seen a strong recovery in employment, but we’re still significantly below pre-pandemic levels.

The point is that if you had told me a year ago that this is what current output and employment numbers would be, I wouldn’t have predicted soaring inflation. To put it another way, my expectations of a relatively muted effect of government outlays on demand were more or less vindicated. But of course my expectations of moderate inflation weren’t. So what happened?

Part of the answer lies in supply-chain issues. Overall demand hasn’t grown all that fast, but fear of face-to-face interactions has skewed demand away from services toward goods, overstraining shipping and in some cases manufacturing capacity. These issues account for a lot of recent inflation, but in a way they don’t worry me too much: The private sector has huge incentives to get stuff moving, so sooner or later supply-chain issues will fade away.

However, it’s not just the supply chain; it’s obvious that we’re now experiencing widespread labor shortages even though employment is still below its prepandemic level.

I mentioned that the employed percentage of prime-age adults has generally been a good indicator of the state of the labor market. Another good indicator is the rate at which workers are quitting their jobs: Quits are high when people believe that new jobs are easy to find. Normally these two measures move in tandem; but something has changed.

Here’s a scatter plot of the prime-age employment rate against the quit rate since 2001; the blue dots represent the pre-pandemic era, the red dots the era since early 2020:

[Krugman has a diagram that I totally fail to understand, so you’ll have to imagine it.]

You can see [or imagine] the close relationship between the two measures [the prime-age employment rate and quit rate] before 2020. Since then, however, the relationship seems to have shifted, so a labor market that seems only OK judging by the employment rate looks extremely tight judging by the number of people who are quitting. And wages are rising rapidly, which suggests that quits are telling the real story.

What we’re seeing, of course, is the Great Resignation — which is also, to an important extent, a Great Retirement. A recent blog post from the International Monetary Fund shows that there has been a surge in the number of older Americans (and Britons) choosing not to be in the labor force. . . .

Now, a labor market in which jobs are easy to find and workers can bargain for higher wages is a good thing. But the fact that labor markets are so tight even though employment and real G.D.P. are below pre-pandemic projections suggests that we can’t rely on those projections to assess the economy’s productive capacity. For whatever reason or reasons — presumably linked to Covid-19 — the U.S. economy apparently can’t sustainably produce as much as we expected [and scarcity means rising prices].

And that in turn tells us that it’s time for policymakers to pivot away from stimulus — in particular, that the Federal Reserve is right to be planning to raise interest rates in the months ahead. As I read the data, it doesn’t call for drastic action: The Fed should be taking its foot off the gas pedal, not slamming on the brakes. But that’s a story for another day.

For now, the moral is that because of Covid-19, we can’t assess where we are simply by comparing our situation with the pre-pandemic trend [i.e. the normal state of affairs]. . . .

Unquote.

In other words, inflation, a global phenomenon, not one restricted to the US, is principally an effect of economies adjusting to a fading pandemic, another global phenomenon, which is not business (or economics) as usual.

You must be logged in to post a comment.