Prof. Paul Krugman explains a few things about Social Security:

The thing about Social Security is that from the beginning it was designed to encourage misconceptions. It looks, on casual inspection, like a giant version of a private pension plan. You pay into such a plan during your working years, contributing to a pension fund, and when you retire, you receive payments from that fund in proportion to the amount you put in….

I haven’t studied the detailed history of the program’s origins, but I’m pretty sure that it was set up to look like an ordinary pension fund because that made it politically easier to sell. But in reality, Social Security has never been run like a private pension plan.

For one thing, for the first half-century of the program’s existence, it had almost no assets; in 1985, the trust fund was only large enough to pay around two months’ worth of benefits. So it has always operated mainly on a pay-as-you-go basis, with today’s payroll taxes paying for today’s retiree benefits, not tomorrow’s.

I often get mail from people claiming that this makes Social Security a Ponzi scheme. But it isn’t. It’s just a government program supported by a dedicated tax, which is fairly common — for example, that’s how we pay for roads and bridges, which are funded by gas taxes.

The other way Social Security is unlike a private pension is that what you get out isn’t at all proportional to what you put in. Workers with low earnings get a much higher share of those earnings replaced than higher-wage workers. In the past, this made the program strongly redistributive — a much better deal for workers with low pay than for workers with high pay.

By the late 1970s, it was clear, however, that Social Security was facing financial trouble down the road. The baby boom ended in 1964, so the working-age population, which grew rapidly as long as boomers were still entering the labor market, would grow more slowly in the decades ahead; this meant that the program’s tax base would grow more slowly than the number of beneficiaries, especially once the boomers began retiring.

So in 1981 a bipartisan commission set out to secure Social Security’s future. It tried to do so with two measures. First, it increased the payroll tax rate; the idea was to make Social Security a bit more like a “real” pension fund by taking in more than it was spending, building up a serious trust fund that could help defray costs once the baby boomers hit the system. It also set in motion a gradual rise in the age of eligibility for full benefits, which started at 65 and will reach 67 for those born after 1960.

All of this was supposed to secure the system’s finances until 2060. It did, in fact, buy the system a number of decades, but the Social Security Administration currently expects the trust fund to be exhausted by 2035. The main reason for the shortfall, as I understand it, is that taxable wages have grown more slowly than expected, which in turn is largely the result of rising inequality: A growing share of overall income has gone to people with really high earnings, and much of that income [anything over $160,200] isn’t subject to the payroll tax….

So what happens once the trust fund is exhausted? The system doesn’t collapse — but payroll tax receipts are expected to be only about 80 percent of promised benefits. So if nothing is done, benefits will suddenly have to be slashed by 20 percent.

That, however, almost certainly won’t be allowed to happen. These programs are both immensely popular and deeply relied on, after all.

One obvious course of action would be to provide the system with more money. I get a lot of mail from people saying that we should simply eliminate the upper limit on the payroll tax. That would certainly raise a lot of money. But bear in mind that there’s no fundamental reason Social Security has to be financed with payroll taxes; we do it that way only because back in 1935, F.D.R.’s advisers thought it would be a good idea to dress Social Security up to look like a private pension fund. And Social Security isn’t the only program that’s going to need more money unless we cut expenses. So we should be trying to figure out the best way to raise a few more percentage points of G.D.P. in taxes. To achieve that, raising the payroll cap may not be the best way to go.

The other idea I hear a lot is that we should raise the retirement age — which has already been increased, from 65 to 67. After all, people are living longer, so they can work longer, right?

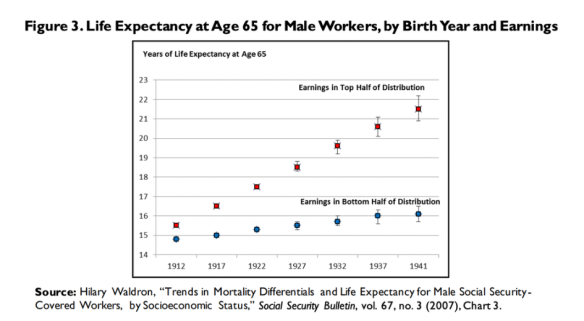

Well, some people are living longer. But one key point in thinking about Social Security is that the number of years you can expect to spend collecting benefits has become increasingly linked to the income you earned earlier in your life. Here’s a chart everyone discussing retirement ages should know about, although many don’t. It shows how life expectancy at age 65 has changed for Americans with different levels of income.

:…. Life expectancy has indeed risen a lot for the affluent, but for the less well-paid members of the working class, it has hardly risen at all.

What this means is that calling for an increase in the retirement age is, in effect, saying that janitors can’t be allowed to retire because lawyers are living longer. Not a very nice position to take.

Growing disparities in life expectancy also mean, by the way, that Social Security isn’t as redistributive as it used to be. Low earners get more of their income replaced than high earners, but this is increasingly offset by the fact that they have fewer years to collect benefits.

In any case, I hope we don’t raise the retirement age further. As I wrote last week, what we need is medical cost control plus moderate tax hikes.

And meanwhile, don’t worry too much about your future benefits. Social Security isn’t a Ponzi scheme, it isn’t going bankrupt, and it will probably continue much as it has.

Meanwhile, an article for Politico suggests a way to protect Social Security that nobody seems to mention.

There are a lot of strange aspects about [the Social Security] debate, but perhaps the oddest is that [everybody acts] as if Social Security is the only part of the U.S. old-age benefit system. The other parts of the system — including defined-benefit (DB) pensions, defined-contribution (DC) plans like 401(k)s, and individual retirement accounts (IRAs) — are rarely mentioned and completely spared from proposals to cut benefits….

According to the Joint Committee on Taxation, the tax advantages for DBs, DCs and IRAs will cost the federal government $371 billion this year…. Given these tremendous [tax breaks], it is initially hard to understand why people who seem so worried about the costs of old-age benefits choose to focus solely on Social Security. But it becomes easier to understand once you realize who benefits the most from the various parts of the old-age system….

According to the Congressional Budget Office, the richest 20% of Americans receive 58.1% of all the government subsidies provided to DBs, DCs and IRAs while the poorest 20% receive just 1.3%….

DBs, DCs and IRAs also provide significant amounts of fee revenue to Wall Street banks and other financial intermediaries who administer the tens of millions of individual accounts and pension funds….

Of course, it doesn’t have to be this way. The rules governing DCs, DBs and IRAs … can be changed just as the rules governing Social Security can be changed. If we are seriously worried about the generosity of old-age benefits or the government’s debt, then everything should be on the table and the part of the system that most favors the rich should be front and center.

For example, … gradually raising the full retirement age to 70 years old … would save $121 billion between 2024 and 2032. However, a similar amount of savings could be achieved by applying an annual 0.03 percent tax on the $34.5 trillion of assets held by DBs, DCs and IRAs…. For a person with a $100,000 IRA, the tax would amount to just $30 per year.

You must be logged in to post a comment.